The UK mortgage industry is vast and growing, with rising house prices even with the overall economic woes. In the current climate, mortgage fraud is still a major issue for banks and lenders.

Valued at £1,667 billion in Q4 2022, British mortgage lending grew at an annual rate of 4.1% last year. With stricter lending criteria being imposed by banks as interest rates rise, some customers are trying to get around the rules.

To help you understand mortgage fraud in the UK market, we’re going to look at:

- The different types of mortgage fraud you may come across;

- Who is most likely to commit UK mortgage fraud;

- How you can protect yourself from mortgage fraud.

What is mortgage fraud?

Mortgage fraud comes in many guises, but it is generally when someone knowingly gives false information to a mortgage lender to borrow money they wouldn’t normally be able to.

The different types of mortgage fraud tend to describe the type of lies that are being told, such as:

- Income fraud – lying about your income to borrow more than you’d be allowed, this includes falsifying P60s and payslips.

- Occupancy fraud – lying about who will be living in the property; owner-occupied mortgages tend to have lower rates than buy-to-lets.

- Property fraud – lying about the condition or value of the property in order to borrow more than it’s worth or reduce the deposit required.

Identity fraud is also an issue that lenders have to deal with.

This could happen in two ways, either someone could pretend to be you and take a mortgage out in your name, or they could pretend to be you to change ownership records at the Land Registry and then borrow against your home.

Who commits mortgage fraud?

In the UK, most mortgage fraud is committed by gangs or syndicates, including property professionals like a solicitor, surveyor, or mortgage broker.

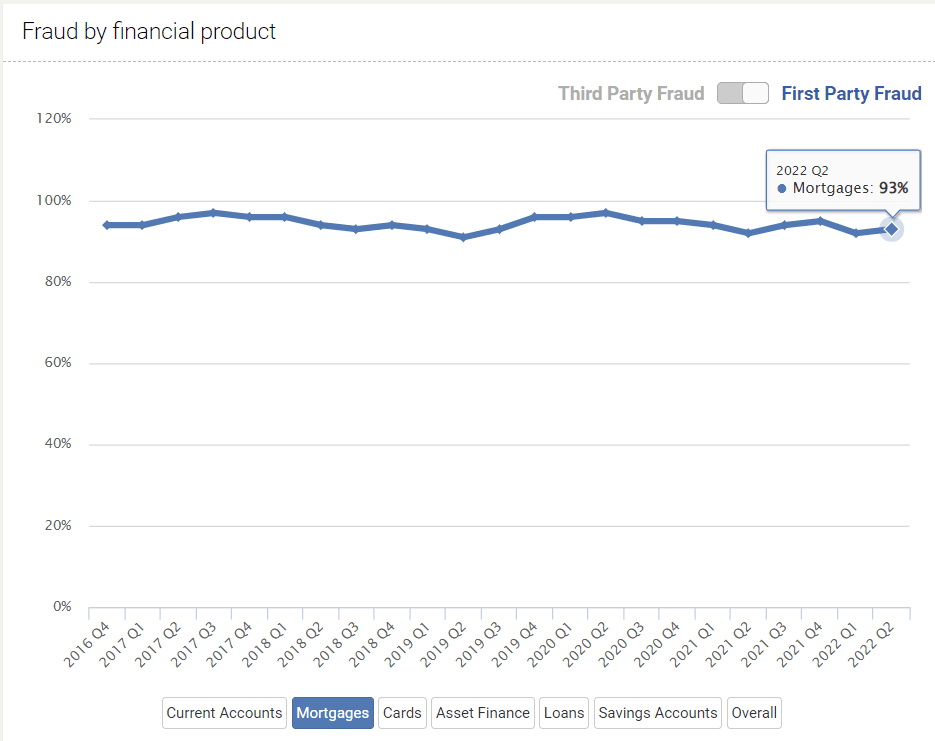

According to data from Experian, one the main credit reference agencies in the UK, first parties committed 93% of mortgage fraud in Q2 2022.

Source: Experian

This means that more than nine times out of ten, the person committing mortgage fraud was the one directly involved in the sale. It’s a common way for criminals to launder money obtained through other types of crime because it is seen as relatively low risk, although it is still a crime.

The other 7% of mortgage fraud is when a person like you falls victim to identity theft. People will pretend to be you to take advantage of your credit score and borrow huge sums of money or take control of your property ownership so they can take a mortgage on your home.

It sounds like a scary prospect, but there are ways you can protect yourself.

How to prevent mortgage fraud

When you come to sell your house, hopefully, it is for positive reasons, and you’re moving up the property ladder.

If you find yourself in financial difficulties or mortgage arrears, you may be approached by companies offering to buy your home in cash with a fast turnaround.

The price will be low compared to the market value, and you may come under pressure to lie about the property condition or value so the money can move fast.

This may sound tempting, but you may be breaking the law. Being aware of this type of scam is move number one in preventing involvement in mortgage fraud.

Chances are, the mortgage fraud you’d more likely run into is identity theft. People get hold of your personal information, pretend to be you, and borrow money that you’re eventually liable to repay.

Here are our top tips on how to prevent mortgage fraud through identity theft:

- Check your credit report often so you can see if any applications have been made in your name and what debts you currently owe.

- Secure your internet browsing using a UK VPN; this will encrypt the data that goes to and from your computer and prevent people from hacking your browsing if you use public WiFi.

- Dispose of your documents sensibly; if you still have paper statements and records, don’t leave them out on bin day – shred them instead.

- Be suspicious of calls or emails claiming to be from the bank; no one will ever ask for security or identifying details on an outbound call. Call the bank back if you’re concerned.

What to do if you’re a victim of mortgage identity theft

If you do come across evidence that your details are being used to take out fake mortgages, you need to act quickly.

- First, you can contact CIFAS, the UK Fraud Prevention Agency to get protective registration – this means whenever a financial search is done under your name, extra checks will be made.

- You will also need to make a report to Action Fraud, which is a police portal to register this type of crime. If you want to make a report over the phone or in person, you can call the police non-emergency line on 111 or go to your local station.

Protect yourself from mortgage fraud

With so many people facing financial pressures in the UK in 2023, mortgage fraud isn’t something that may be at the front of your mind. It’s more important than ever to keep on top of your personal data security and watch your credit report, so stay vigilant.